- North Carolina LLC vs. Sole Proprietorship

North Carolina LLC vs. Sole Proprietorship

What is an LLC?

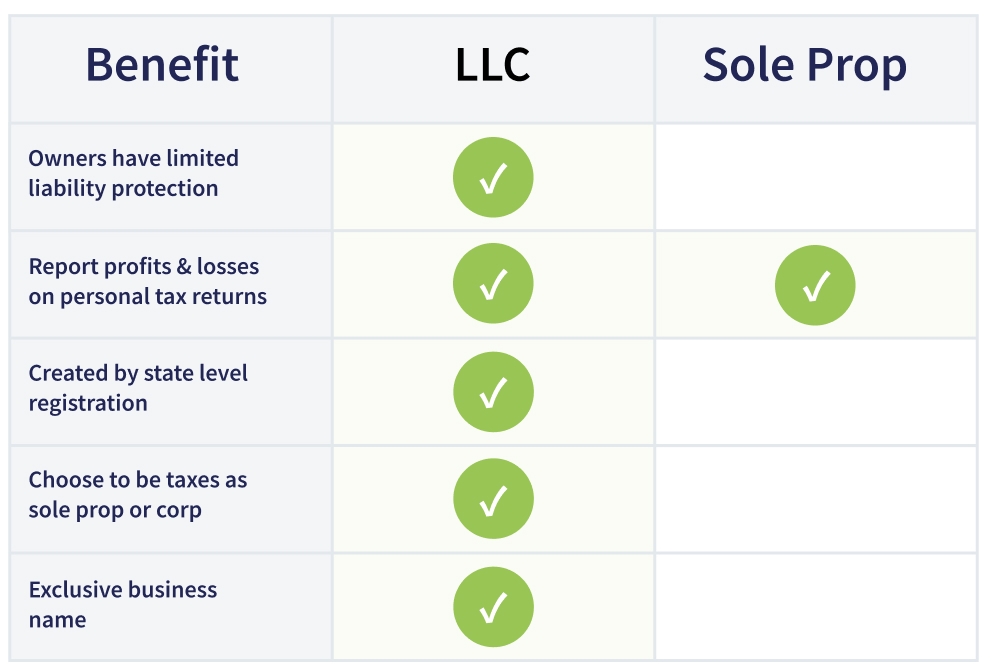

A limited liability company (LLC) is a business structure whereby the owners are not personally liable for the company's debts or liabilities. It is a relatively new hybrid business structure in most states, including North Carolina.

What are the advantages and disadvantages of an LLC?

LLCs have several advantages, including tax savings, liability protection, privacy (if formed anonymously), increased credibility, and improved tax flexibility. One potential drawback is the added complexity when compared to a sole proprietorship. A list of the pros and cons for LLCs is shown below.

Pros:

- LLCs have a lot of flexibility when it comes to organizational and managerial decisions. LLC members can structure the company in almost any way they deem helpful.

- LLCs can also be managed by company members or by an appointed manager.

- In addition, LLCs can decide how they will be taxed. One option for taxation includes pass-through taxation. This taxation option is where individual members report LLC profits on their income tax returns. More information on taxation options is available below.

- LLCs do not have to follow the same stringent corporate regulations required when operating corporations.

- There are no limitations on how many members or who may be an LLC member.

Cons:

- There are more tax options available for LLC companies. This can cause increased complexity and difficulty navigating the best options.

- Across state lines, tax and liability treatment is not the same.

- There are some limitations on transferring LLC ownership.

- LLCs are required to use accrual basis accounting methods. This method records revenues and expenses before payments are received or issued.

What does it cost to set up an LLC in North Carolina?

To establish an LLC in North Carolina, you must file the articles of organization. The cost to submit these documents to the secretary of state is $125.

What is a Sole Proprietorship?

A sole proprietorship also referred to as a sole trader or a proprietorship, is an unincorporated business with just one owner who pays personal income tax on profits earned from the business. Most small businesses start as sole proprietorships. It is the most straightforward type of structure to run your business. The business is treated as an extension of the owner. In other words, unlike LLCs, no legal distinction is made between the owner and the business. There are no necessary steps or paperwork you need to submit when operating a sole proprietorship. However, many people submit a “doing business as” request with their local county clerk’s office and obtain a Certificate of Assumed Name to take on an assumed name such as “Sprinkles and Cakes.” Without this certificate, the sole proprietorship must operate under the owner’s name, for instance, “Jackie’s Cupcakes.” For more information about assumed business name filing, you can visit North Carolina’s Secretary of State website.

What are the advantages and disadvantages of a sole proprietorship?

There are several advantages to sole proprietorships, including mainly the convenience and simplicity of the business structure. Although sole proprietorships offer freedom and flexibility initially, they can also come with financial risks later down the road for the owner. Below is a detailed list of the pros and cons of running a sole proprietorship.

Pros:

- The most straightforward and least costly form of business structure

- Maintenance costs are minimal

- Sole proprietorship owners have freedom and control over their business decisions within the limitations set by law.

- Business profits go directly to the owner. Taxation is, therefore, simpler; the owner can simply file their tax return and not worry about taxation at the business level.

- It is relatively easy to convert a sole proprietorship to a different business structure. This can be particularly advantageous once the business grows and the owner desires protection from personal liability for the business’s debts or obligations.

Cons:

- Sole proprietorship owners have direct liability for all the debts against the business. The business and personal assets of the owner may be at risk.

- There is also potential for higher tax rates for this business entity as everything is considered earned income.

- Owners are at a disadvantage when it comes to raising funds. They may often be limited to using funds from their personal savings account or consumer loans.

- It may be challenging to attract well-established employees with experience compared to larger organizations or those who desire the opportunity to become official business members.

- As the only business owner, the demands and pressure lie only on you.

- The business entity dissolves when the owner passes away or retires.

What is the difference between the two?

There are several categories to help distinguish between sole proprietorships and LLCs. These include liability, taxation, and management/ operational style.

Liability

Generally, sole proprietors own small or part-time businesses with no employees. It costs nothing to establish a sole proprietorship. Unlike a sole proprietorship, an LLC is a hybrid of the partnership and corporate forms that allows the liability protection of a corporation with the tax advantages of a partnership. As hinted above, this is a crucial difference between the two business structures. Sole proprietors are not protected from personal liability.

Taxation

Another essential difference between LLCs and sole proprietorships is tax flexibility. Only LLC members can choose how they prefer to have their business taxed. Only LLC members can choose how they prefer to have their business taxed. They can also elect to have corporate tax status. Dividends are taxed at a lower rate than typical business income when the company is taxed as a corporation. Corporation retained earnings are also not subject to income tax. LLC members must pay taxes on all business income, whether retained or not. A corporation has eligibility for additional tax deductions and credits.

Management and Operations

A sole proprietorship is simple in its operations and management structure. The single owner can make any business decision as they see fit. Most sole proprietors can hire employees, experts, and other individuals to help with day-to-day choices with business management. However, the owner only has to ensure that their business operates legally and that the profits cover business expenses.

An LLC's operational and management structure is more intricate. Often it is outlined in an LLC operating agreement. The operating agreement details each member's stake in the business, voting rights, and profit share. The LLC can be collectively managed by all the members or an appointed manager. North Carolina does not require you to submit the operating agreement to their secretary of state, but it is recommended nevertheless. It can help resolve disagreements later down the road more quickly.

LLC & Sole Proprietorship taxation differences?

Suppose you operate your business as a sole proprietor. In that case, you’ll be taxed as a self-employed person, and the income of your business is considered your personal income for tax purposes.

An LLC may make an election to be taxed as a disregarded entity, partnership, corporation, or s-corp. Note that if you elect to be taxed as an s-corporation, North Carolina taxes you at a rate of 5% of the annual profits and you have to pay additional franchise taxes. If such an election isn’t made, it’s taxed as either a disregarded entity or a partnership, depending on the number of members it has.

Should You Start an LLC or Sole Proprietorship?

Business owners often start with sole proprietorships. It requires minimal paperwork and is simple in design, as shown previously. Once the business grows, transitioning to LLC may have the advantage of offering protection against personal liability for bankruptcy.

Those who want personal liability protection, tax benefits, growth potential, credibility, and consumer trust should strongly consider forming an LLC. It is recommended for businesses with more extensive customer bases, increased risk of liability and/ or loss could potentially benefit from unique tax options and have the possibility for immediate sustainable profit. One immediate downside is the fees and more complex formation process than sole proprietorships. However, this can easily be made up for with the benefits your business can assume by establishing your company as an LLC.

Sole proprietorships work well for small-scale, low-risk, and low-profit businesses. Therefore the risk on an owner’s assets is minimal. The best business structure will depend on many factors, and it's recommended that you speak to a business lawyer before deciding.