Wyoming LLC Taxes

Fair Market Value and Limited Liability Company Units

The tax laws concerning LLCs change on a regular basis. New opportunities are regularly created, and some opportunities may be lost. Therefore, do not look at your LLC plan as something you do and then forget. It is a business. Like any other business, it requires regular attention.

To understand the tax consequences of using an LLC in Wyoming, it is important to define “fair market value” (FMV) and its relationship to the LLC. FMV is defined in Treas. Reg. 20.2036-1(b) as:

When a willing and fully informed buyer pays a willing and fully informed seller, both are free to say no and both have any facts relevant to the transaction.

The LLC agreement itself limits the economic value of an LLC unit by restricting the rights of members. For example, the agreement may state that a Member has no right to demand a distribution, order dissolution of the LLC, participate in the management of the LLC, withdraw from the LLC, or sell his or her LLC units to anyone without a 100% vote of all members. Thus the Member’s interest is not as valuable as the representative share of underlying assets since he or she lacks the rights of a full owner.

Full value is represented by the actual asset or fraction thereof, that the member would own if there were no LLC. Since this is not what the member has, LLC units are “discounted” to a more reasonable fair market value at death to reflect this marketplace reality, i.e. that they are not “worth” full value on an ongoing basis. An informed buyer would not ordinarily be willing to pay as much for LLC units as for a comparable asset without restrictions on the enjoyment of LLC in Wyoming benefits.

Potential Transfer Tax Reduction

When LLC units are given as gifts, they are valued for gift tax purposes at their fair market value. If the fair market value of the LLC units has been determined by a competent appraiser to be less than the fair market value of the underlying assets due to LLC agreement restrictions, the donor of the gift may actually transfer more value using LLC units. For example, should the LLC units be discounted by 1/3, a gift of $10,000 of LLC units is equivalent to the gift of $15,000 in underlying assets. ($15,000 x 2/3 = $10,000)

Intergenerational Wealth Planning and Transfers

The LLC is a business entity that can carry on any permitted business activity. This makes it a flexible tool for planning. A Wyoming LLC structure can facilitate wealth planning in several ways.

(a) Family as a Wealth Collaborative

Many American families keep their financial affairs totally secret, yet expect other family members to manage for them should they become disabled or die. This is especially problematic given the great number of businesses that are family-owned, of which 40% are in transition at any time with little or no planning. Also, one of the common issues in American families is the fear that as children mature they will drift away or move away from the family. Senior family members are rightfully concerned about the availability of credit and the temptation to create a lifestyle using it. LLCs are investment tools.

A powerful non-tax reason for creating a family business enterprise is that it can be used to train and prepare family members for success in their investment lives. Many of our clients use an LLC as a “kitchen table” mechanism to retain control while providing a forum for family financial and investment planning. This “glue” can help keep the family together. Information critical to the well-being of family members can be shared. Using a business structure in the form of an LLC as a means of creating effective communication and financial goal-setting for the family is one of the primary benefits of this form of planning.

(b) Ease of Gifting

Gifting fractional interests in certain investment assets can be difficult and problematic. For example, a farm, real estate, or business is hard to split into fractional interests. To complicate matters, some asset values change on a daily basis. The LLC allows for gifts of fractional interests of the LLC itself since LLC units are similar to shares of stock. The LLC owns the underlying asset while members own LLC units or a percentage of the entity. A person assigns a share or part of a share in order to transfer units.

(c) Gift Tax Savings

The law allows annual gifts, within limits, to be made without paying gift taxes. The limit on such gifts is $13,000 per gift recipient per year as of 2007. (Check with your attorney or tax accountant as this exclusion may change in future years.) If one spouse makes a gift and the other spouse joins in the gift, the annual gift tax exclusion increases to $26,000 per year per gift recipient. Thus, a couple with four children may give away up to $104,000 per year in cash or in kind without using any portion of their lifetime exemption from estate and gift taxes.

Valuation discounts generally apply to fractional interests in any business, including a family business, whether active or passive. For example, if a valuation discount of 50% applies to LLC units, then a single person making gifts of LLC units could effectively remove $26,000 in comparable asset value from his or her taxable estate each year per gift recipient. With that type of discount, a couple with four children could conceivably gift the equivalent of $208,000 each year in related underlying assets, by gifting $104,000 of LLC units.

(d) Death Tax Savings

The valuation adjustments discussed above may also apply to the remaining LLC units of any deceased member. % of ownership x FMV x (1 - discount) = Estate Tax Value

(e) Protection of Gifted Interests

Outright gifts of cash or other property can be problematic. The assets or cash gifted may be wasted, lost to creditors, or lost in divorce. It is difficult to give a fractional interest in property other than cash. Accordingly, ownership of LLC units with transfer restrictions can protect the integrity of the LLC structure and its underlying assets from being lost or wasted by the gift recipients. LLC units cannot be spent, wasted, or obtained by creditors. Restrictions in the LLC agreement can prevent the transfer of LLC units to those outside the LLC without the agreement of all members.

(f) Alternative Income Options vs. LLC Distributions

General Members are entitled to income in the form of management fees as compensation for managing the LLC. LLCs can be structured with a “preferred equity interest” that pays a set percentage of income to holders of that interest. These potential income sources can provide security to certain members even though they may have given away a substantial percentage of LLC units.

Maintaining Control Over LLC Activities

Clients may serve as managing members or simply as managers of the LLC. Sometimes an entity manager is advisable for continuity of management since entities do not become disabled or die. A management trust, LLC, or corporation could be considered, and even a third-party manager under contract. Should a manager-based LLC be created, the control of a manager could include full control over investment decisions, including decisions about how much LLC income to distribute or to reinvest inside the LLC entity, or far less than that degree of control. Generally, however, a manager answers to the members. Note, however, that a member-manager must act in a fiduciary capacity in exercising management authority.

Income Tax Attributes of Using an LLC

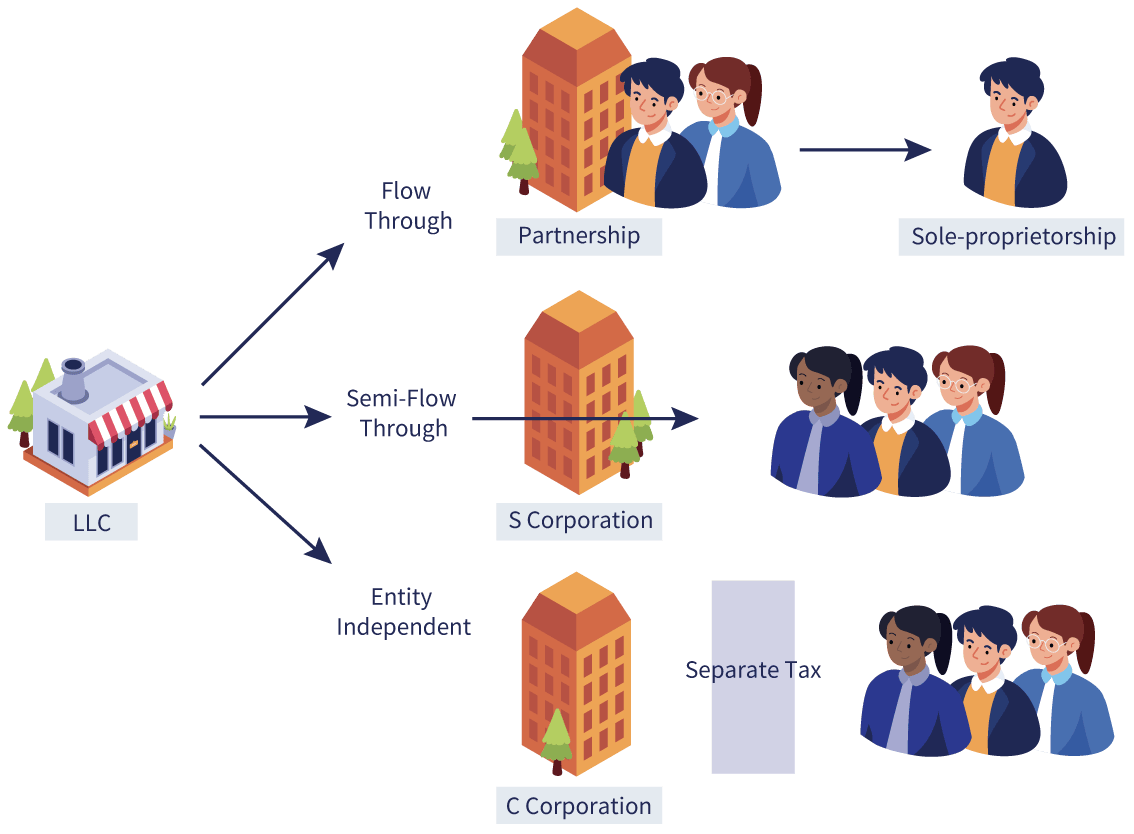

An LLC with two or more members by default is taxable as a partnership, i.e. a flow-through entity for income tax purposes. This means that members receive their portion of the income tax attributes of the LLC. The LLC will file an IRS Form 1065 income tax return but does not pay income taxes. However, it may also elect taxation as a C or S corporation. Similarly, a sole member LLC may be taxable as a disregarded entity or as a C or S corporation but not as a partnership.

Transfers of property to an LLC are normally not taxable events. Typically the transfer of property into an LLC by an individual is a capital contribution, and the person making the transfer of assets into it receives LLC units (a percentage of ownership) in exchange for the contribution. Finally, upon dissolution of an LLC, the distribution of assets to members would in most cases not trigger an income taxable event since it would usually be a return of capital. There are some exceptions to these general rules on dissolution of the LLC and those exceptions are largely dependent on entity tax status, so the situation should be reviewed at that time. Even if there is no tax on dissolution, there could be capital gains tax consequences when distributed assets are later sold.

Income Tax Savings Using an LLC

The use of the LLC may result in income tax savings through the use of income shifting to members in lower income tax brackets.

Franchise Tax Savings Using an LLC

In some jurisdictions, there are franchise tax savings associated with LLCs that are not available to other business entities. However, in some jurisdictions, LLCs are taxed more heavily than other forms of business ownership. State income tax and franchise tax laws must always be considered. Learn more about Wyoming LLCs here.

How Does the LLC Transact Business?

All important transactions of the LLC, such as major business agreements, loans, employment agreements, leases, and buy-sell agreements, must be considered and approved by formal action of the Members unless authorized by a Manager. If there is a pattern of individual action without the necessary formalities, the members involved risk a legal determination that they were acting and are liable as individuals, despite their use of the LLC name. The end result could be a loss of tax benefits and asset protection.

What About Taxes on Wages and Salaries?

The Wyoming LLC and its managers, officers, and members are responsible for the payment of salaries, wages, and payroll taxes. They must ensure that salaries and wages as well as payroll taxes are properly paid. They may incur personal liability if the LLC fails to make proper withholdings and tax payments.

Must the LLC Withhold Taxes on Wages or Compensation Paid to Employees?

Employers, who pay taxable wages to employees or who have employees who report tips, must withhold income tax and Social Security (FICA) taxes. Each employee should fill out a Form W-4, withholding allowance certificate, or form W-4E, exemption from withholding. Every employer must file all necessary Form 941 quarterly employment tax reports by the last day of the month following the end of each calendar and an annual unemployment tax return, Form 940, on or before January 31 of each year.

Is the LLC Required to Withhold State Income Taxes?

The Limited Liability Company must normally comply with any state withholding requirements in all states in which it does business.

Obtaining Distributions from the LLC

There are four ways to obtain cash from an LLC.

- First, the managers of the general member can be paid management fees for managing the LLC. If the general member is an entity, the entity can use the management fee to pay salaries to its managers.

- Second, distributions (of income) may be declared. When distributions are declared, all limited members receive a pro-rata share of the distributions.

- Third, the LLC can make loans, at market interest rates, to the limited members or to the general members. The note signed upon the creation of a loan, and any unpaid interest, is a legitimate debt for the taxable estate of the borrower if the loan is not paid back prior to death. Such outstanding loans can reduce the estate tax of the borrower.

- Fourth, when distributions are paid, limited members could use the distributions to purchase more LLC units from the founders of the LLC should they desire to sell some of their LLC units. Since these sales are at the fair market value (FMV) of the LLC units, this sale will get more LLC units out of the founders’ taxable estate, provide a source of cash to the founders, and allow the founders to “freeze” the value of their taxable estate to some degree.

Does Transferring an Asset Into the LLC Create Tax Liability?

There is normally no tax owed when the property is contributed to the LLC in return for an LLC interest. The transfer of assets to an LLC in exchange for an LLC interest is called a capital contribution. If someone sells property to the LLC, however, the seller must pay any taxes (such as capital gains tax) resulting from such sale. It is important that you review several of the prior articles of this manual for the exceptions to this tax-free transfer rule!

The Role of the LLC Accountant

Ideally, a CPA should be involved prior to or immediately following the decision to consider entity planning. The CPA is sensitive to income tax planning and compliance issues, valuation issues, and integration of the entity design into the comprehensive wealth and estate plan.

Deductibility of Fees Paid for Business and Estate Planning

Legal and tax advice fees for business planning is usually deductible in the year that the fees are paid. Estate planning fees for certain services may be tax deductible. Fees paid for the organization of the LLC may be amortized over a period of 60 months from the date the LLC is organized. An election under section 709 of the Internal Revenue Code will need to be made on the first federal income of the LLC. These possible deductions should be reviewed with your income tax return preparer.

Filing of Income Tax Returns

The LLC must file an annual federal income tax return on IRS Form 1065. Many states also require annual state income tax returns for entities. Tax accounting is very complex, and the services of a good tax CPA should be seriously considered to prepare the LLC tax returns. When taxable as a partnership, or as a disregarded entity, income, losses, and other tax attributes from the LLC will flow through to the members on a pro-rata basis, absent special planning provisions usually referred to as “special allocations.” Different rules may apply if the LLC is taxable as a corporation.

Federal and State Securities Laws

The LLC could be subject to federal and state securities laws. It is important for your attorney and CPA to make a determination whether or not they apply. If they do, it is essential that all sales and offers to sell any LLC units are made in compliance with both federal and state securities laws. Failure to comply can result in serious consequences.

Learn about the benefits of a Wyoming LLC here.

Because of the complexity of the legal requirements relating to disclosure and registration of offering securities, it is most important that legal advice be obtained when any financing plan is developed and prior to any contract with any person concerning the possible sale of any LLC interests. If matters are not properly handled from the outset, opportunities for financing may be legally foreclosed. Note, that taxation is not decided in the operating agreement.

Conclusion

Wyoming LLCs offer a range of benefits, from flexibility in business operations to potential tax savings. Control over LLC activities and income tax attributes can be leveraged effectively. Establishing and managing your LLC requires ongoing attention to compliance and proper planning. For articles of organization, annual report, EIN, bank account, or business search, see our Form a Wyoming LLC pages.

If you're ready to establish your Wyoming LLC and require guidance, please reach out to us. A member of our Business Success Advisor team will assist you. You can either fill out the contact form or dial +1 (307) 683-0983 to connect with us.