- Living Trust

Revocable Living Trusts in Wyoming

Revocable, Anonymous & Avoids Probate

WY Revocable Living Trust (RLT) Overview

The revocable living trust has been a significant estate-planning tool for many years and is the foundation for most estate plans in Wyoming. For that reason, it is important for people to understand how a Revocable Living Trust works, the advantages of the arrangement, and most importantly, whether the advantages are applicable to their particular circumstances.

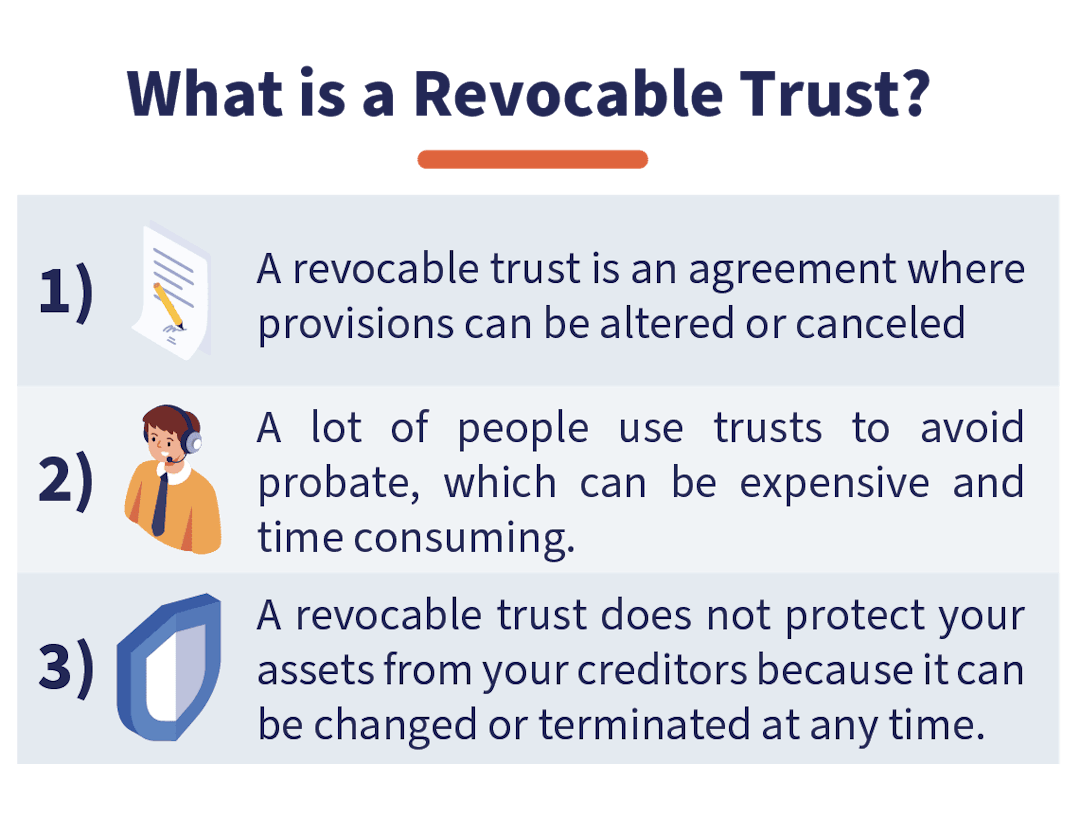

A Trust is an agreement between the individuals who establish the Trust, called the trustors, settlors, or grantors, and the individual(s) or company who will manage the Trust’s assets, called the trustee. The individuals or organizations who receive the benefit from the assets in the Trust are called the beneficiaries. A Trust is called a Living Trust if it is a Trust established between a trustor and a trustee while the trustor is still alive, as opposed to a Testamentary Trust which is established pursuant to a person’s Last Will and Testament and becomes effective upon the person’s death.

A Living Trust can either be revocable or irrevocable. If it is a Revocable Trust, the trustor can change the terms of the Trust and/or revoke the Trust completely at any time during his/her lifetime and competency. However, if the Trust agreement provides that the Trust is irrevocable, the trustor is not legally entitled to amend or revoke the Trust. While Irrevocable Trusts are utilized in estate planning to some extent, the vast majority of Trusts are revocable Living Trusts. Interested in knowing more? Discover whether an Irrevocable Wyoming Trust is a good fit for you.

While a Revocable Living Trust has a number of advantages, the two primary reasons for establishing Trusts of this type are:

- Avoiding the probate of the trustor’s estate

- Establishing a manner of distributing assets to beneficiaries

Avoidance of Probate

With just a Will, the assets of a decedent’s estate will have to detour through probate court before those assets are distributed to the decedent’s beneficiaries. In very general terms, probate is designed to ensure that a decedent’s debts are paid and that the decedent’s assets pass to his or her beneficiaries in accordance with the decedent’s Will (or if the decedent did not leave a Will, then in accordance with intestate succession laws). Probate expenses in Wyoming generally approximate 5% to 10% of the gross probate assets. However, if a person is diligent in transferring title to all of his or her assets to a Revocable Living Trust prior to death, there would not be any assets titled in that person’s name at his or her death. As a result, there would not be any assets of the decedent required to go through the probate proceeding.

Please note that in order to avoid a probate proceeding, the trustor must transfer the title to all of his or her assets to the Living Revocable Trust during the trustor’s lifetime, and ensure that all life insurance proceeds and retirement plan assets which pass according to beneficiary designations upon his or her death are not payable to his or her “estate.” This transfer process generally requires the actual recording of new deeds for real estate, changing the name on bank and stock brokerage accounts, partnership interests, etc., and reviewing and possibly changing beneficiary designations on insurance and retirement assets.

Following the transfer of assets, the trustee (who is normally the same individual as the trustor) transacts business involving the Trust’s assets in the name of the Revocable Living Trust; however, the Revocable Living Trust does not have to obtain a separate federal tax identification number (unless the trustee is not the same person as the trustor), nor does it need to file separate income tax returns, because all the income of the Trust is simply reported by the trustor under the trustor’s social security number.

While probate proceedings can be avoided with a Revocable Living Trust, it is important for individuals with substantial estates to understand that even if a Trust is fully funded with all the decedent’s assets, there will still be professional fees incurred for the preparation of the estate tax returns, the administration of the Trust, and the allocation of the Trust’s assets to the subtrusts which are established following the trustor’s death.

Additional Probate Considerations

In addition to the primary benefits of a Revocable Living Trust discussed above, there are other features of this type of Trust that may be beneficial to trustors. For instance, in the event a trustor becomes physically or mentally incapacitated, the Revocable Living Trust may eliminate the need for a conservatorship proceeding, and thereby permit the uninterrupted management of the trustor’s assets by the named successor trustee(s) without any court interference. This includes helping manage a limited liability company.

Further, when a Will is probated, the contents of the estate and distribution scheme of the Will, as well as a list of the decedent’s assets, may become a matter of public record. In contrast, the provisions of a Revocable Living Trust and a disclosure of its assets are not filed with the probate court (regardless of whether or not there is a probate). Finally, since the Revocable Living Trust is simply an agreement between the trustors and the trustees, who are often the same individuals, it is very easy to make modifications or changes or revoke the agreement entirely, without the formalities required by statutes for other testamentary documents.

Joint Wills

Most people want to plan for what happens to their money and property after they pass away. This is where a Will comes in. A Will allows an individual to state their intentions about how their assets should be distributed after they die.

If you die without a Will, the state will appoint someone to distribute your assets according to the state's intestacy laws, which may or may not be what you want.

Married couples sometimes decide to create a joint Will to dictate how their assets should be distributed after one or both passes away. But, while a joint Will may seem like a great idea at the time it is executed, it can easily result in unwanted consequences later on.

What is a Joint Will?

A joint Will is one that is executed by two individuals, most commonly, a married couple. Typically, a joint Will provides that when the first spouse dies, the surviving spouse will inherit everything and then when the surviving spouse dies, everything will pass on to their children or other third parties.

A joint Will is effectively a contract between the two spouses that can only be changed, restated, or revoked in accordance with contract law, which will require a "meeting of the mind" or, in other words, a mutual agreement between the spouses.

The Problem with Joint Wills

Because no one knows for certain what the future will bring, there are a number of things that can go wrong with a joint Will. For example, what if you and your spouse have a disagreement in the future?

A joint Will cannot be unilaterally revoked by either party. Furthermore, once the first spouse dies, a joint Will becomes irrevocable—unable to be changed or revoked by the surviving spouse at all.

However, many things can change between the time the Will was executed and the death of the first spouse, and just as many things can change after. For example, what happens if the surviving spouse remarries and/or has more children?

In either of these situations, the joint Will may no longer reflect the needs or wishes of the surviving spouse for the distribution of his or her estate. But, because one of the parties to the joint Will has died, there can no longer be any meeting of the minds. Therefore, the surviving spouse will be unable to change the Will to provide for his or her new spouse and/or children.

Moreover, what if:

- The surviving spouse needs to sell the home that he or she shared with the deceased spouse in order to pay for long term care?

- The surviving spouse relocates to a different state and needs to amend the Will to reflect the legal requirements in the new state?

- A beneficiary proves to be financially irresponsible or falls into drug or alcohol addiction after the death of the first spouse and the surviving spouse wishes to change the distribution scheme to prevent that beneficiary from squandering their inheritance?

- The surviving spouse simply wants to change a beneficiary or the executor named in the joint Will?

In each of these circumstances, the surviving spouse will be unable to make the desired or necessary changes to the joint Will and this may ultimately result in their estate being distributed in a manner that does not reflect what is needed or desired.

Consider the following scenario:

You are married with two stepchildren, but no children of your own. When your marriage was going well, you and your spouse executed a joint Will to provide for each other and then your stepchildren. Later, however, your marriage fails and you find yourself divorced and estranged from both your ex-spouse and his or her children.

In this case, you may no longer wish for your ex-spouse's children to inherit from you. However, unless your ex-spouse agrees to allow you to change the joint Will to disinherit his or her children, which is highly unlikely, your former stepchildren will still inherit from your estate when you pass away. What's more, if your ex-spouse dies before you, you will have lost even the possibility that the joint Will could ever be changed.

Why a Revocable Living Trust May Be a Better Option Than a Joint Will

Joint Wills are rather outdated concepts and don't reflect the current status quo—marriages are less likely to last a lifetime, blended families are much more common, and individuals and families relocate more frequently.

Today, the use of other estate planning tools, such as a revocable living trust, are better options for directing the distribution of a couple's estate after they pass away. In fact, each of the problems above can be avoided by a revocable living trust.

A properly drafted revocable living trust will allow a couple to express their wishes for the distribution of their estates, while enabling those wishes to be updated as circumstances change.

Also, unlike a will, a revocable living trust is effective during the creator's lifetime, and can be used to manage the family's assets while the creator is alive and well, when they are alive but incapacitated, and after they pass away.

What's more, assets held in the name of the trust avoid probate, saving time and money and facilitating a much faster transfer of assets to loved ones.

Consult with an Experienced Estate Planning Attorney

Creating an effective estate plan would be relatively straightforward if we could accurately predict the future. But no one knows what the future holds.

Consequently, a comprehensive estate plan is far more than having a certain estate planning document in place. You need a personalized plan that prioritizes your goals, but one that can easily be updated as those goals change.

Not everyone will need a Revocable Living Trust. If you believe it suits your needs or are looking for more information about estate planning, including Wills, Trusts, and other estate planning instruments, consult with an experienced estate planning attorney.